.jpg)

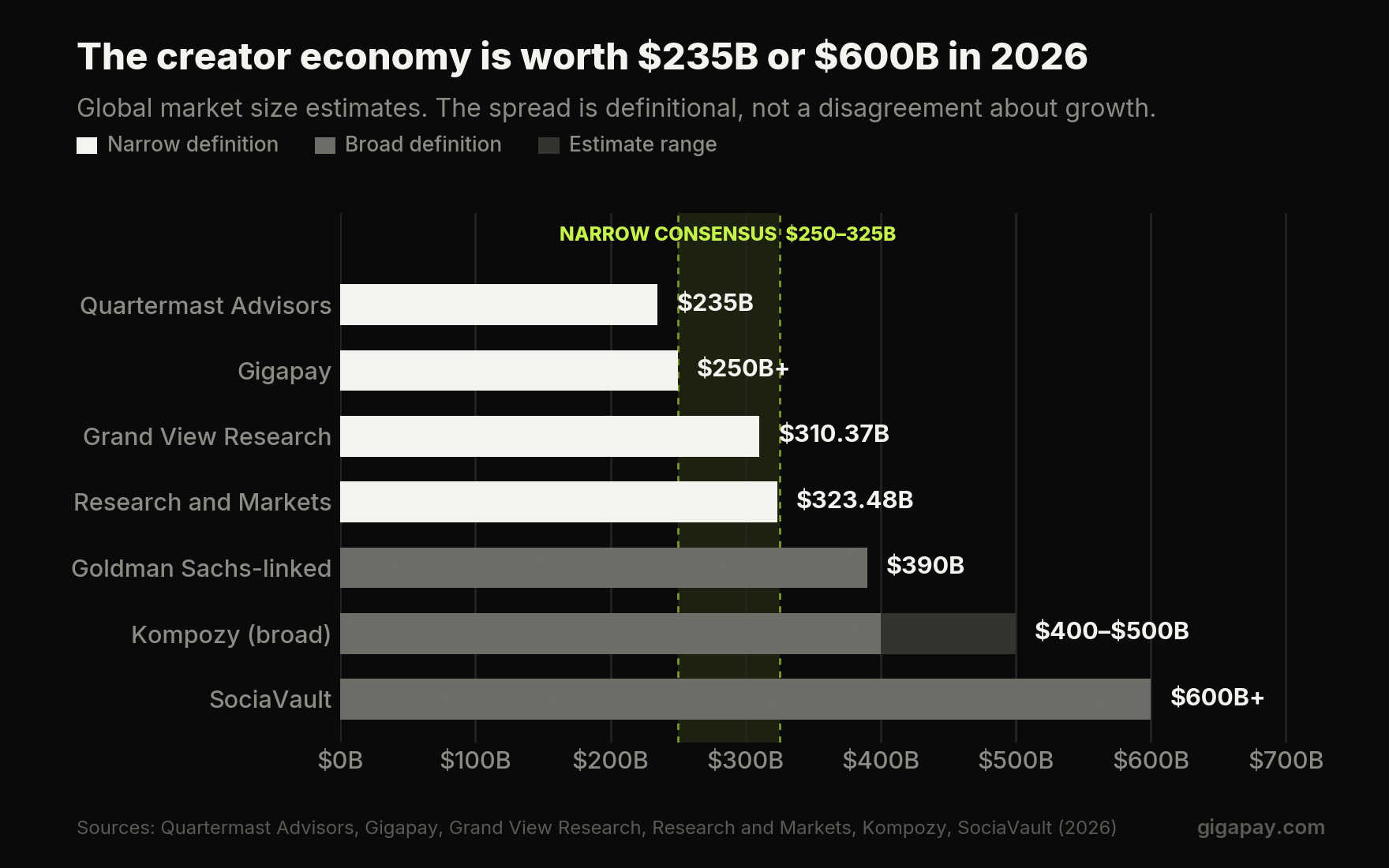

Six credible research firms published a 2026 size for the creator economy this year. Their answers range from $235 billion to more than $600 billion. All six are defensible. None of them are measuring the same thing.

That spread is the most honest place to start a report like this, because it tells you something the headline number cannot: the creator economy has grown faster than the ability to describe it. There is no census. There is no agreed unit of account. A market that moves roughly a third of a trillion dollars a year through more than 200 million people still has no shared definition of what counts.

This report compiles what the 2026 data actually supports, across market size, creator population, earnings, platform economics, social commerce, brand spend, AI adoption, capital flows, and the operational layer underneath all of it.

Gigapay built this report because we sit on the payment layer. Brands publish budgets. Platforms publish user counts. Very few people publish what it costs to actually move money to a creator, on time, across a border, without breaking a tax rule. That is the part we can see, so that is the part we measured most closely.

Methodology and Sources

This report compiles data available as of July 2026. Full-year 2026 actuals do not exist yet, so figures draw on early-to-mid-2026 surveys, platform disclosures, and forecasts covering either 2025 actuals or 2026 projections. Each is labelled as such.

Limitations you should read before the numbers

Creator earnings are gross and largely self-reported, which means they behave like ranges rather than salaries. Survey samples skew toward creators who already identify as professional, which pushes averages up. US-based surveys carry most of the granular earnings data, so global extrapolation is imperfect. And market-size figures depend entirely on definitional scope, which is where this report starts.

Key Findings

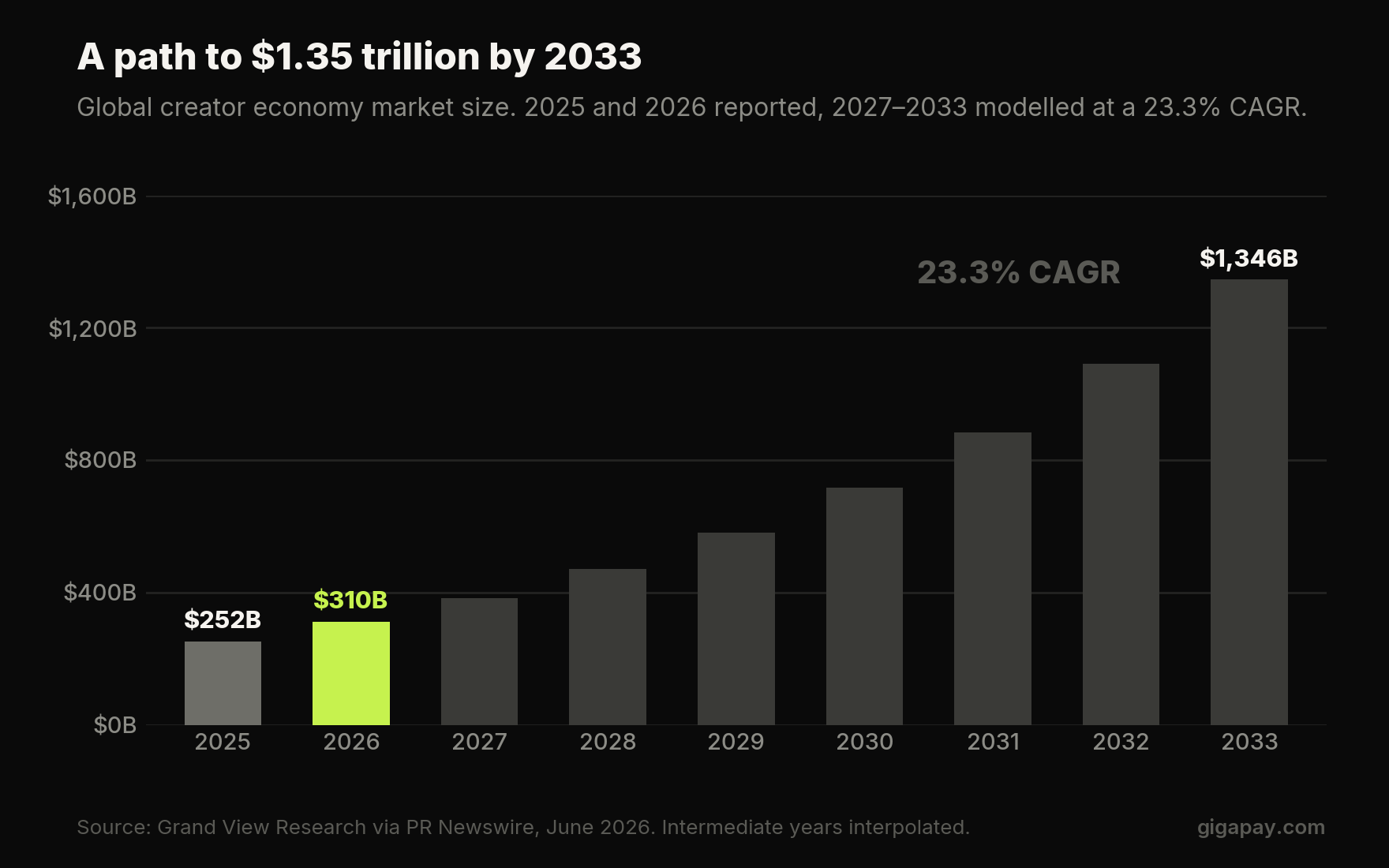

- The global creator economy sits somewhere between $235 billion and $600 billion in 2026, depending on whether you count direct creator revenue or the full ecosystem around it. The narrow consensus clusters at $250–325 billion.

- Grand View Research projects $310.37 billion in 2026, up from $252.33 billion in 2025, with a 23.3% CAGR carrying the market to $1.35 trillion by 2033.

- More than 200 million people create content. Roughly 50 million do it professionally or semi-professionally. About 2 million earn six figures.

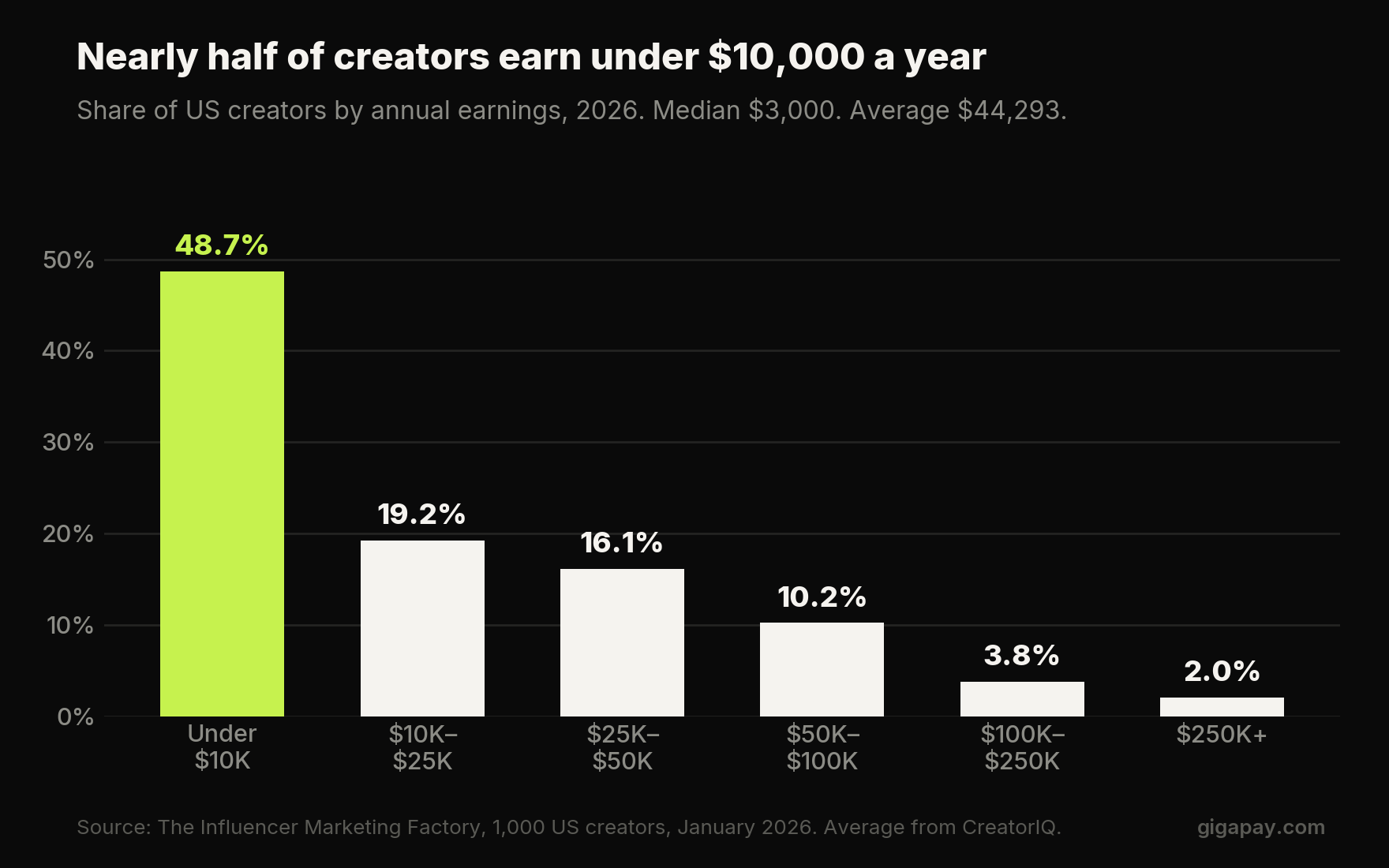

- 48.7% of creators earn under $10,000 a year. The median is roughly $3,000. The average is $44,293. When the mean runs fourteen times the median, you are looking at a power law.

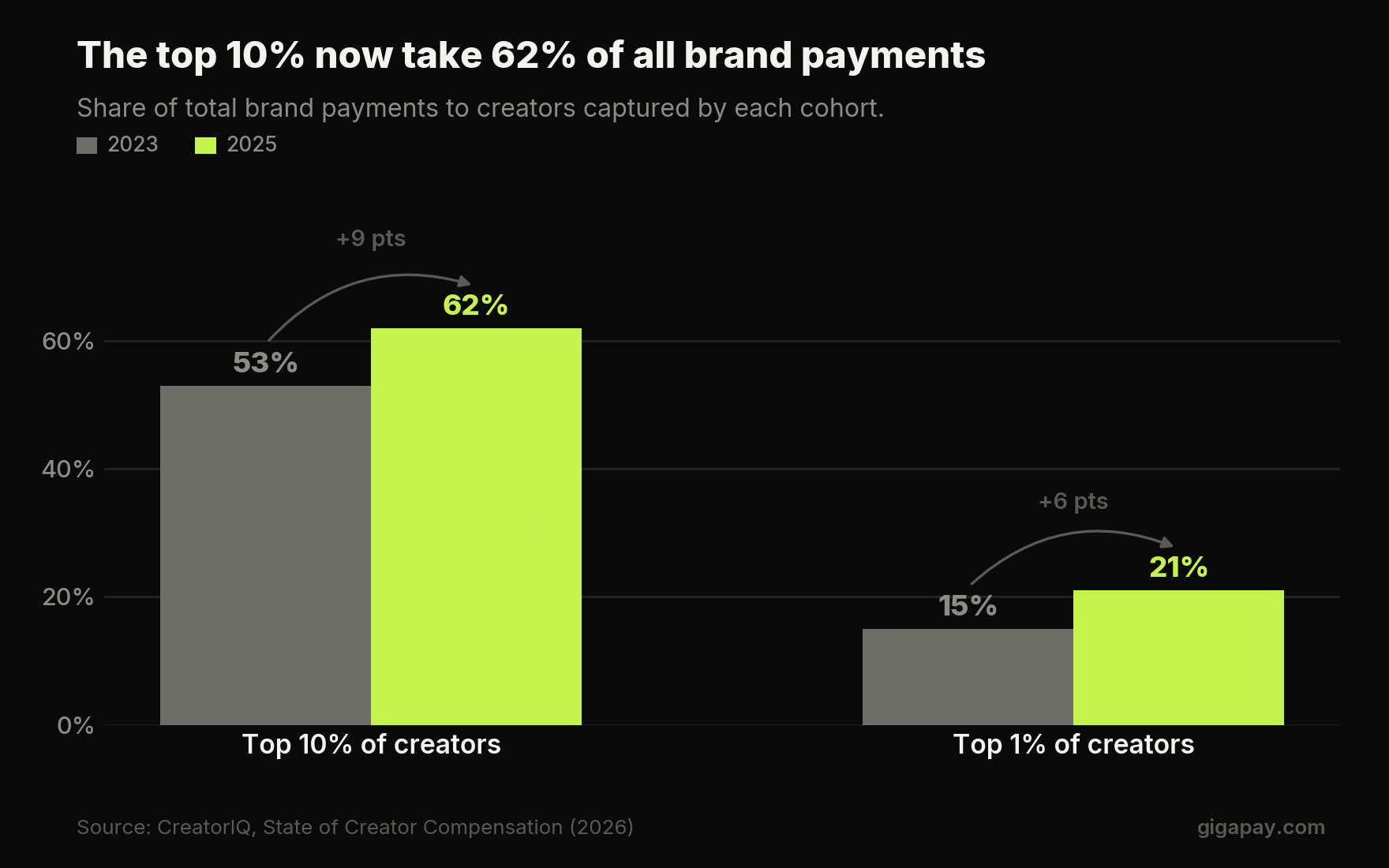

- The top 10% of creators captured 62% of all brand payments, up from 53% in 2023. The top 1% moved from 15% to 21%.

- Brand spend on creators reached $32.6 billion in 2026. Creators are projected to keep more than $21 billion of it.

- 87.49% of marketers expect budgets to rise in 2026, and 72.22% expect increases of 50% or more.

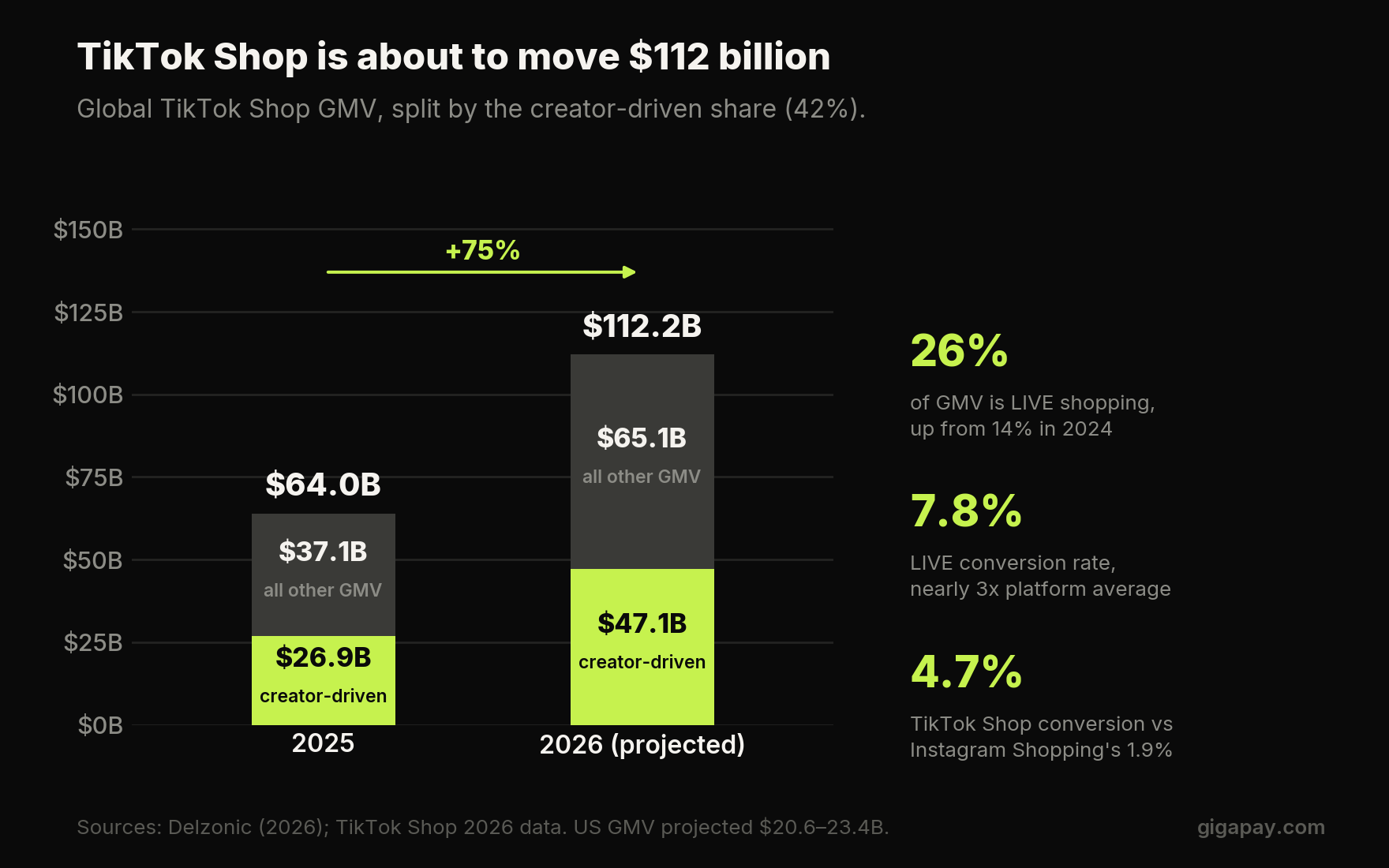

- TikTok Shop GMV is projected at $112.2 billion globally, nearly double 2025. Creators and affiliates drive about 42% of it.

- 70 M&A transactions closed in H1 2026, up 23% year over year, alongside $1.291 billion of disclosed equity funding across 28 rounds in the twelve months to June.

- 75% of creators describe AI as integrated or essential to their work, and pure AI-generated content prices 40–60% below human equivalents.

- Between 52% and 78% of creators report burnout, and 69% report financial insecurity tied directly to how unpredictably they get paid.

- Payment delays still reach 120 days.

The Size and Shape of the Market

Why the number you quote depends on who is asking

Before any 2026 market size means anything, you have to know which of two questions it answers.

- The narrow definition counts money that lands in a creator's hands: sponsorships, platform payouts, product sales, subscriptions, affiliate commissions, services.

- The broad definition counts the whole ecosystem: creator-driven ad spend, commerce GMV attributed to creators, the software they buy, the platform inventory their content sells against, the agencies and tools built around them.

Kompozy's mid-2026 analysis puts narrow at $200–300 billion and broad at $400–500 billion. SociaVault, using the widest lens available, estimates ecosystem-wide activity above $600 billion in 2026, up from roughly $480 billion in 2024. Both are describing the same industry.

That is why a CFO reading "$600 billion creator economy" and a CFO reading "$235 billion creator economy" can both be correct and reach opposite conclusions about how much budget to move. The number is a definition, not a measurement.

How big is the creator economy in 2026?

Here is the full range on the table, narrow to broad:

The cluster is real. Strip out the two extremes and five of seven estimates land between $235 billion and $390 billion, which is a tighter agreement than the headline spread suggests.

The growth curve to 2033

Growth is the more interesting number. Grand View Research models a 23.3% CAGR from 2026 through 2033, reaching $1.35 trillion. Kompozy reads year-over-year growth in the 10–20% band, down from the 20–30% peaks of the early 2020s. Both readings can hold at once, because a maturing market compounds slower in percentage terms while adding more absolute dollars than it ever has.

Where the money sits inside the market

Grand View Research's segment data, using a 2025 baseline that carries into 2026, breaks the market down like this:

- Individual content creators are the largest end-use segment at 57.2%.

- Advertising is the largest revenue channel. Subscriptions are the fastest-growing.

- Video streaming dominates by platform.

- Photography and videography is the largest creative service category.

The one to watch is subscriptions. Advertising still pays the bills, and the fastest-growing channel is the one creators control, which shows up again in the income-streams data further down.

The Creator Population

How many creators are there worldwide?

More than 200 million people worldwide create content in some economic sense. SociaVault puts the 2026 figure closer to 250 million. Kompozy gives a range of 50–300 million and explains the width honestly: the answer depends entirely on whether "creator" means anyone who has ever monetised a post or someone who files taxes as one.

The professional layer is far thinner. Roughly 50 million creators work at it professionally or semi-professionally. About 2 million earn six figures a year. Kompozy estimates that only 4–5% of the total population earns primary or full-time income from creating.

The earnings pyramid

SociaVault's 2026 tier estimates give the clearest shape of the pyramid:

Each step up costs you an order of magnitude of the population. Roughly one creator in a thousand who earns anything at all clears half a million dollars.

What Creators Actually Earn

How much does the average creator earn in 2026?

The Influencer Marketing Factory surveyed 1,000 US creators in January 2026. It remains the most granular look at individual creator income published this year:

Nearly half of all creators earn under ten thousand dollars a year. A combined 45.6% now earn between $10,000 and $100,000, which is the closest thing the industry has produced to a creator middle class, and its existence is the genuinely new development of the past two years.

CreatorIQ puts the average creator's earnings at $44,293. The median campaign pays about $3,000. That gap of roughly fourteen times is the entire story of creator pay in one comparison, and it means every "average creator earns $44,000" headline you read this year describes almost nobody.

For context on what sits at the top of that distribution: 56% of full-time US creators still earn below the US living wage of around $44,000.

Creator pay concentration is widening, and it is measurable

CreatorIQ's compensation data tracks the concentration directly:

Nine points of share moved to the top decile in two years. SociaVault, measuring total creator revenue rather than brand payments alone, reads the top 1% at roughly 60% of all revenue, with the 90th–99th percentile taking another 25% and the bottom 90% splitting the remaining 15%. The two figures look contradictory and are not: CreatorIQ measures a slice of the market, SociaVault measures the whole thing including platform payouts and commerce, where concentration runs harder.

Payments to creators grew 59% year over year in 2025. More money entered the system and a larger share of it landed at the top. Both facts are true.

Here is the part that matters for anyone running a program. The concentration is partly an artefact of operations. Brands are not paying the top 10% because the top 10% perform best. They are paying the top 10% because paying one creator with two million followers requires one contract, one vendor record, and one invoice, while paying two hundred creators with ten thousand followers each requires two hundred of everything.

The money pools at the top because the top is cheap to administer. That is a fixable problem, and the brands that fix it get to spend where the engagement actually lives.

The very top of the market

Forbes released its 2026 Top Creators list in June, covering roughly March 2025 to March 2026:

- The top 50 collectively earned $1.02 billion, passing a billion dollars for the first time. That is up 20% from $853 million the prior year and 80% from $570 million in 2022.

- Combined following across platforms reached 3.6 billion, up 7% from 3.37 billion.

- MrBeast holds first place at $300 million across 873 million followers.

- Dhar Mann ($65M), Steven Bartlett ($52M), Markiplier ($38M), and Rhett & Link ($37M) round out the top five.

Fifty people earned a billion dollars. Roughly 200 million people earned the rest.

How Creators Make Money

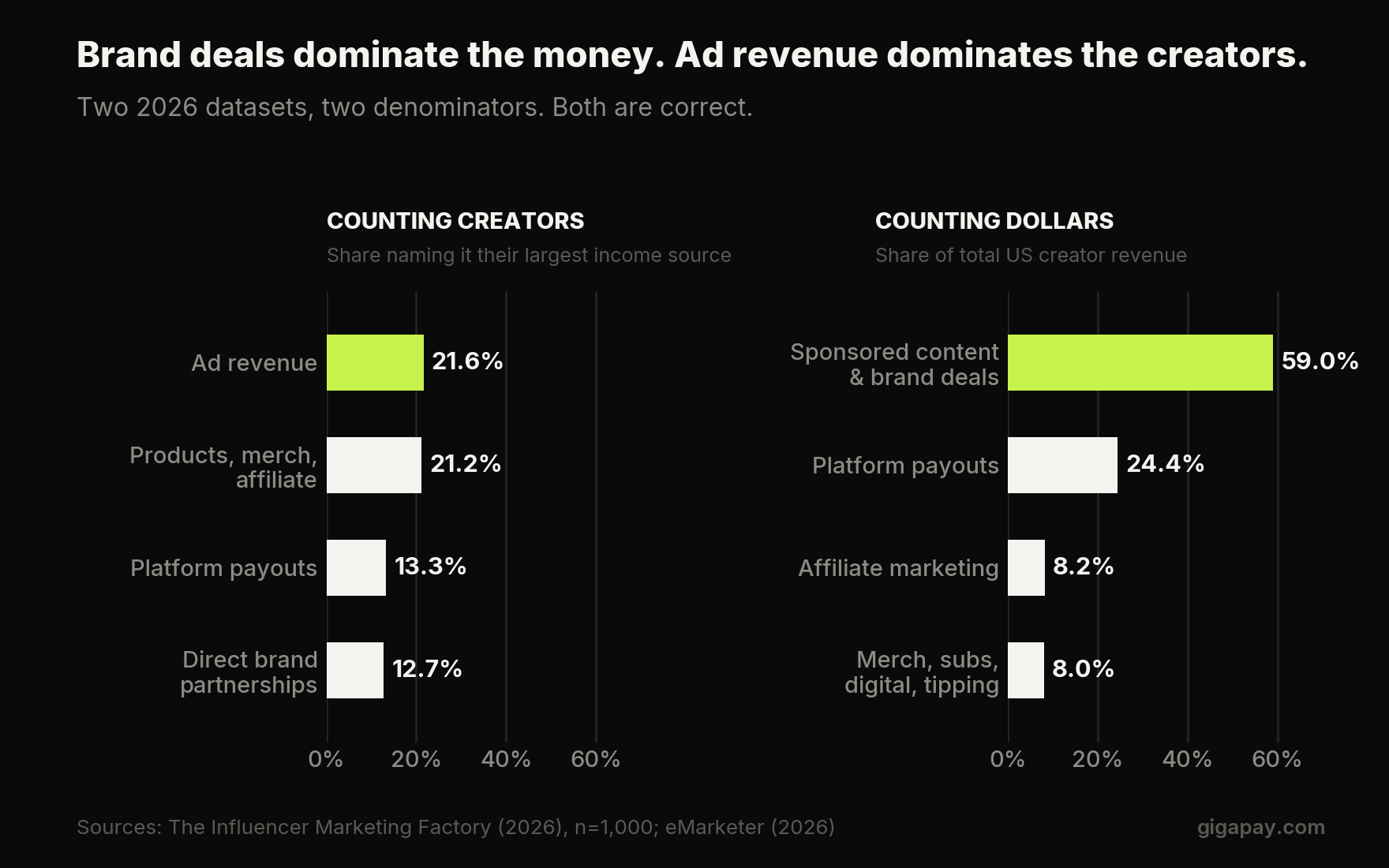

Two datasets, two answers, one useful conclusion

Two credible 2026 sources describe creator income mix and appear to contradict each other completely.

The Influencer Marketing Factory asked creators to name their largest income source:

They are measuring different denominators. IMF counts creators. eMarketer counts dollars. The gap between them says that brand deals dominate the money while a broad base of creators lives on ad revenue and product sales, which is exactly what a power-law market looks like from two different angles.

The move toward income creators own

The direction of travel is consistent across every 2026 source. Creators who last stop depending on the next campaign and start building assets they control.

Circle's 2026 community data quantifies why: 88% of community builders monetise through memberships, and creators with dedicated communities generate 40% more recurring revenue and 3x higher retention than platform-only creators. Community income is projected to become a major or majority share of earnings for many full-time creators by the end of 2026.

The 2026 Creator Signals report found the share of creators prioritising saving money jumped from 32% to 76% in a single year. Creators started behaving like businesses, and businesses want revenue that arrives on a schedule.

Platform Economics

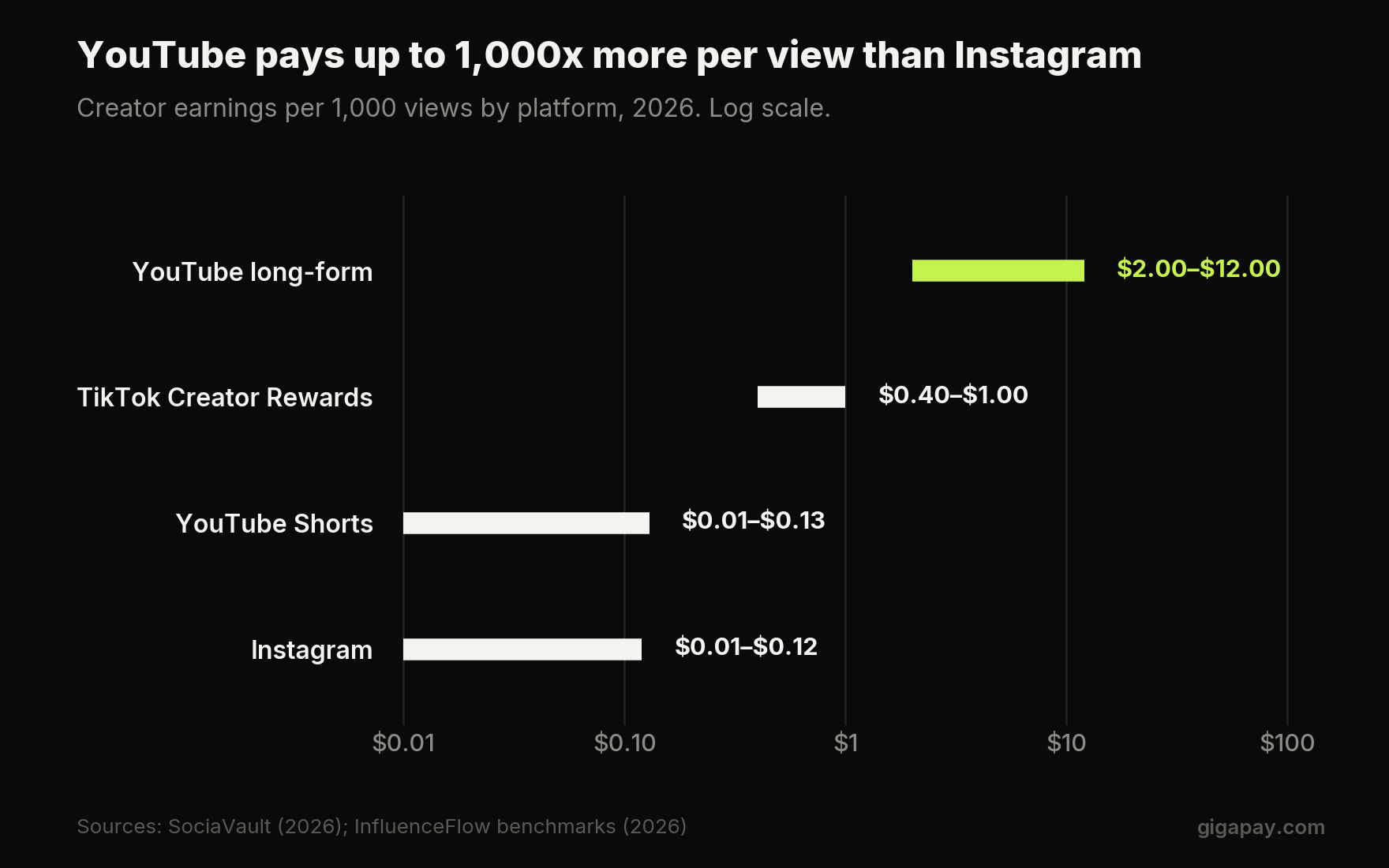

Which platform pays creators the most per view?

Reach does not convert to income at a fixed rate. What a creator keeps depends almost entirely on where the views happened.

Estimated total 2026 platform payouts tell the same story at scale: YouTube around $25 billion, TikTok's Creator Fund, Rewards and Shop affiliate combined approaching $12 billion, Instagram around $8 billion. YouTube's cumulative payouts have passed $100 billion historically. Patreon has crossed $10 billion lifetime.

The recurring-revenue platforms run on different physics. Patreon now pays roughly $24 million a month to between 286,000 and 332,000 paid creators, more than $2 billion a year. Substack has more than 17,000 writers earning income, with mid-tier newsletters commonly bringing in $2,000 to $10,000 a month. LinkedIn sits at the far end with no routine creator payouts at all, where creators monetise entirely through sponsorship and consulting at CPMs reaching $60–$120 in tech and AI niches.

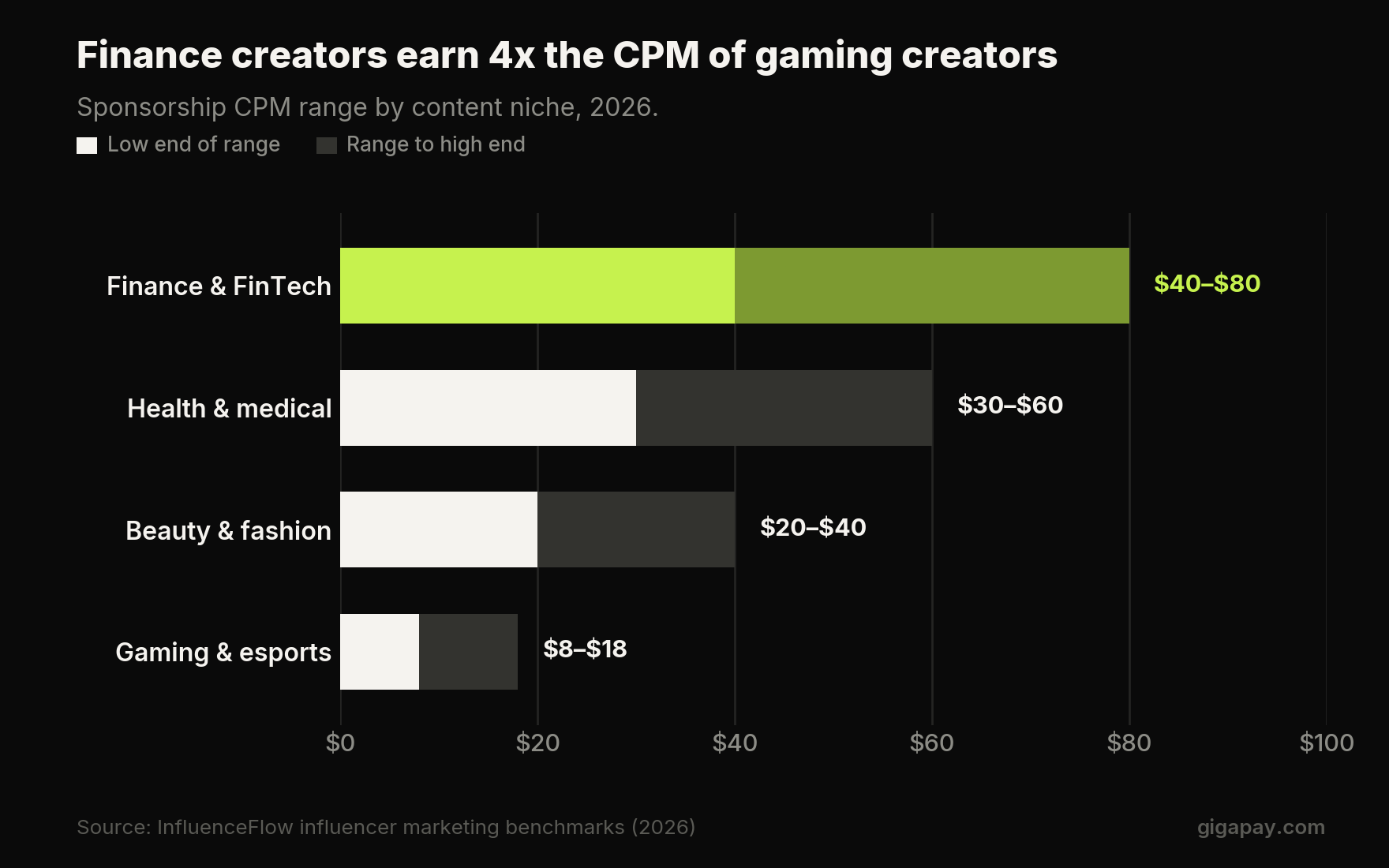

Which content niche pays the highest CPM?

Audience value drives sponsorship CPM, and the spread across niches is wider than most brands price for:

A finance creator with 50,000 followers can out-earn a beauty creator with 500,000, because the brand paying the finance creator is buying a customer worth thousands of dollars. Beauty and fashion, despite carrying the volume, has dropped on saturation. For creators choosing where to build, niche moves income harder than size does.

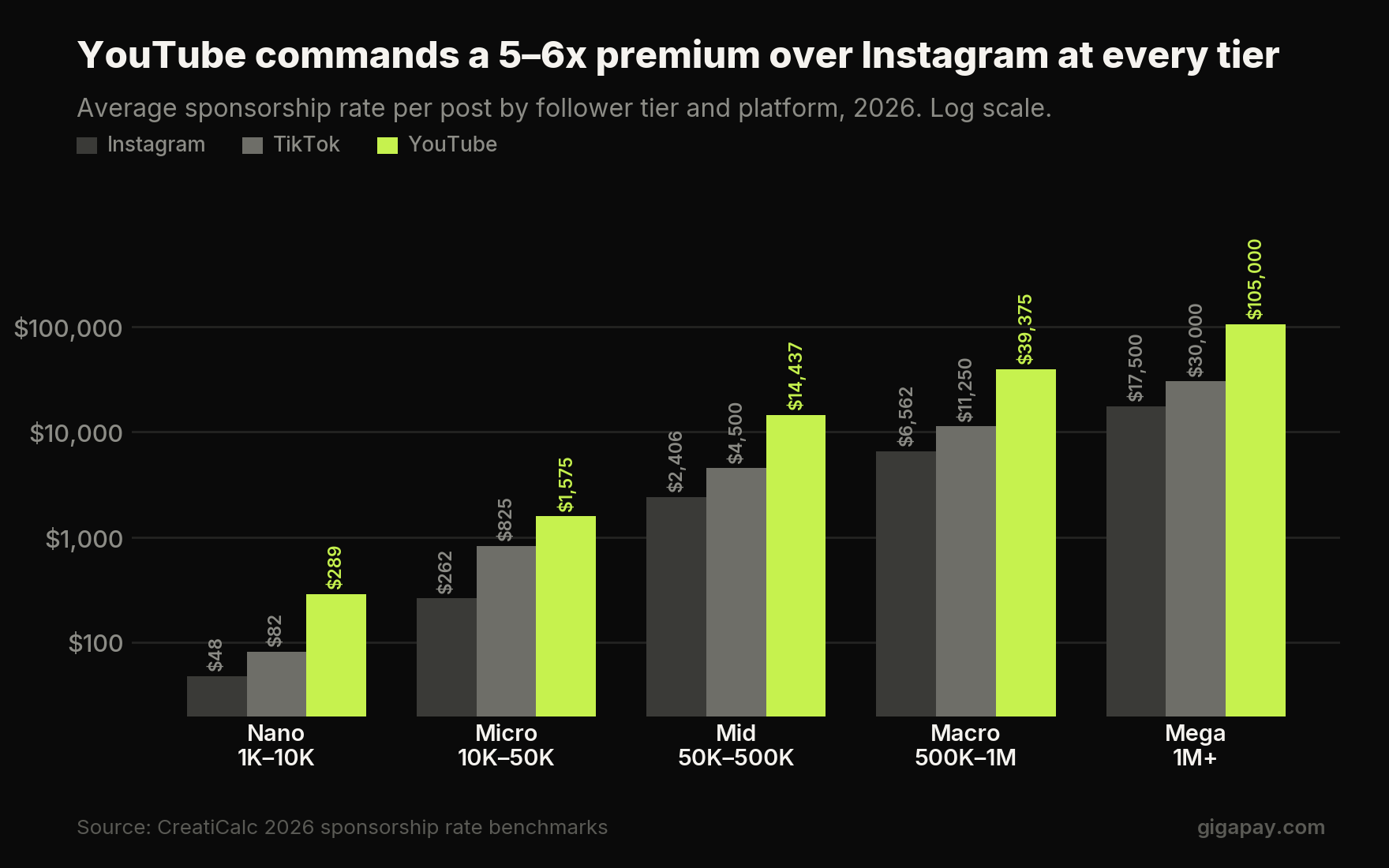

Sponsorship rates by tier and platform

Blended 2026 benchmarks put nano creators at roughly $50–$500 per post, micro at $500–$5,000, mid-tier at $5,000–$25,000, macro at $25,000–$100,000, and mega above $100,000. Broken out by platform, the averages are more useful:

YouTube commands a five-to-six times premium over Instagram at every tier, which reflects production cost, watch time, and intent.

Engagement runs in the opposite direction from price. Nano creators see engagement rates of 8–12%. Mega creators frequently fall below 2%. The audience that costs least to activate is often the one actually paying attention.

This is why brand money is moving down-market. Micro and nano creators claimed 45.5% of all influencer marketing spend in 2026, according to eMarketer, and Traackr's performance data shows nano creators delivering the strongest year-over-year gains in engagement.

There is a catch that every enterprise brand runs into at the same point. The cheapest, best-performing campaigns generate the most payees. A €500,000 program spent on mega creators is five contracts. The same budget spent where the engagement is might be a thousand. Each one is a vendor to onboard, a tax record to file, and a person waiting to get paid.

Platform scale and where the influencers are

Monthly active users, 2026 estimates: Facebook ~3.1 billion, Instagram ~3 billion, YouTube ~2.5 billion, TikTok ~2 billion.

HypeAuditor's 2026 study of 215,000 Singapore accounts gives a rare look at influencer density by platform, and the split is stark. TikTok carries roughly 156,000 influencer accounts to Instagram's 58,000, about three times as many. The gap concentrates at the bottom of the pyramid: 140,000 nano influencers on TikTok against 43,700 on Instagram. Instagram holds slightly higher engagement rates in some tiers.

Visibility remains brutal regardless of platform. Roughly 76% of TikTok posts receive under 1,000 views.

Social Commerce

How big will the TikTok Shop be in 2026?

If one channel defines creator income in 2026, it is social commerce.

TikTok Shop reached $10 billion in US GMV faster than any marketplace in US history.

The conversion advantage is what is moving budgets. TikTok Shop converts at roughly 4.7% against Instagram Shopping's 1.9%, about two and a half times better.

The creator side carries the same concentration as everything else in this report. More than 100,000 creators sit in the affiliate program and around 54,000 clear $10,000 in GMV. The top 0.5% generate 38% of all affiliate revenue. Average US commission runs around 13%.

Meta is building the same road from the other direction

Meta's partnership ads, which let brands turn creator content into paid media, hit a $10 billion revenue run rate in Q1 2026, more than double the prior year. That is a signal worth sitting with. The fastest-growing creator revenue line on the largest social platform is not a payout to creators at all. It is brands buying the right to amplify what creators already made.

Brand Spend and Budgets

How much are brands spending on creators in 2026?

Brand spend on creators reached $32.6 billion in 2026, up from the $24–32 billion range across 2024 and 2025, with some benchmarks projecting as high as $40.5 billion. Of that, creators are projected to keep more than $21 billion.

The IAB's US-specific numbers, measured on a broader ad-spend basis, run higher: $37 billion in 2025, up 26% from $29.5 billion in 2024 and nearly triple the $13.9 billion of 2021, with one analysis projecting around $44 billion for 2026. On the narrowest US definition, influencer marketing spend reached about $10.52 billion in 2025. Three numbers, three scopes, one direction.

Budget intent is close to unanimous

CreatorIQ found average annual influencer budgets grew 171% year over year, with 71% of organisations increasing creator investment, most of it pulled from traditional paid and digital channels. The Influencer Marketing Hub's May 2026 benchmark, surveying 600+ marketers, found 87.49% expect budgets to increase in 2026 and 72.22% plan increases of 50% or more. The IAB found 48% of buyers now treat creators as a "must buy", third behind paid search and paid social.

What brands are getting back

The Influencer Marketing Hub puts average return at $5.78 for every $1 spent, with top programs reaching $18. Payback expectations have compressed hard: 65.9% of marketers expect returns within one month.

Compensation is professionalising alongside it. 53% of brands now use performance-based compensation, and only 6% report not compensating creators at all.

What a creator program costs as a line item

For DTC brands running active programs, creator spend typically runs 2–3% of total revenue, reaching 3–5% in beauty and supplements and often staying under 2.5% in home goods. Creator marketing has become a standard budget line rather than an experiment, which is precisely why the operational questions underneath it now reach the CFO.

TikTok leads investment intent at 31% of marketer selection. Video, short and long form, remains the most effective format. 46.67% of brands plan social commerce tests in 2026, with TikTok Shop leading among adopters.

AI in the Creator Economy

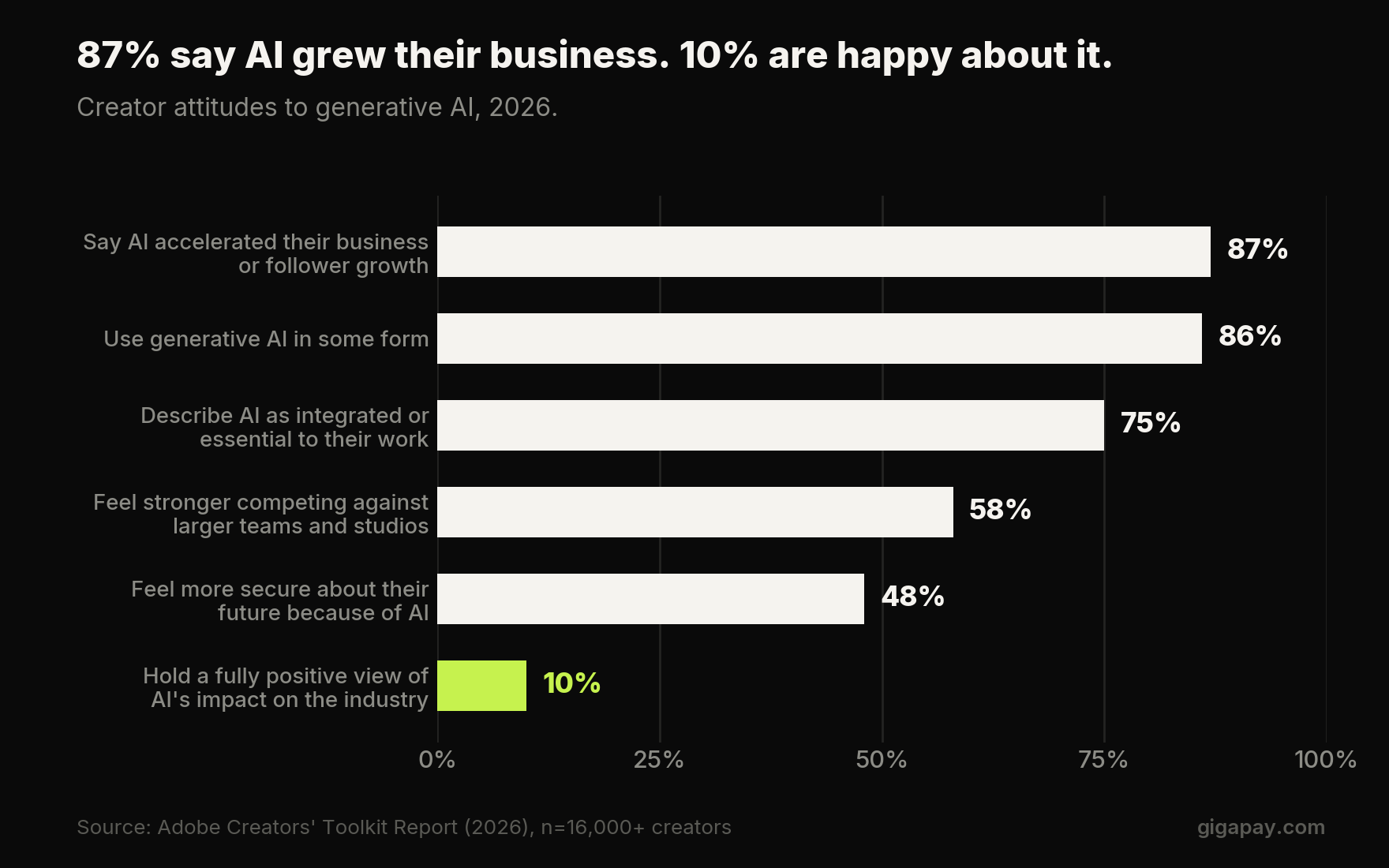

Adoption is effectively complete

Adobe's 2026 Creators' Toolkit report surveyed more than 16,000 creators across multiple countries and found adoption at a level that ends the debate:

- 75% describe creative AI as integrated or essential to their work.

- 87% say AI has accelerated the growth of their business or following.

- 58% feel stronger competing against larger teams and studios because of it.

- 48% feel more secure about their future as a creator.

Separately, 86% of creators report using generative AI in some form, and 56.1% believe it will significantly change how they work. On the brand side, roughly 75% are using or planning AI for creator-related tasks. The Influencer Marketing Hub benchmark breaks brand usage down to creator discovery (36.67%), content generation (21.11%), and brief development (13.89%).

The sentiment is not what the adoption numbers suggest

Only 10% of creators hold a fully positive view of AI's impact on the industry. The same tool that 87% say grew their business is the one 42% blame for making it harder to stand out, with 53% citing sheer content volume as the barrier.

Both things are true at the same time, and the reconciliation is straightforward. AI made every individual creator more productive and made the aggregate market more crowded. The tool that helps you also helps everyone competing with you.

What AI does to rates

The pricing effect is direct and already visible in contracts. Pure AI-generated content prices 40–60% below human-made equivalents. Hybrid work, pairing human strategy with AI execution, sits only 15–30% lower and is emerging as the premium middle ground.

A parallel market is forming. Virtual and AI influencers earn $3,000–$30,000 a month for typical operators, with top accounts reaching $50,000–$200,000 by stacking subscriptions, brand deals, and affiliate revenue.

Capital Markets

M&A hit record pace in H1 2026

Quartermast Advisors counted 70 M&A transactions in the first half of 2026, up 23% on H1 2025, which recorded 86 deals across the entire year. The market is on track for a record.

CAA and TPG launched Compound Creative, a $250 million holding company built to acquire and operate creator businesses across talent, production, tools, and brands.

The pattern across all of it is consolidation and convergence. Traditional media, consultancies, and private equity are buying the creator economy's infrastructure rather than competing with it. Creators are producing theatrical films. Agencies are being absorbed into consultancies. The industry entered what Quartermast calls its third decade and started behaving like a mature one.

Funding tells a more selective story

New Market Pitch tracked 28 disclosed equity rounds by pure-play creator economy companies in the twelve months ending June 2026, totalling $1.291 billion at an average of 2.33 deals a month. Content production software, heavily AI-driven, took 35.7% of deals but 72.6% of the capital. A single June 2026 round accounted for roughly $400 million.

Read against a separate count of roughly $58 million across 9 deals in early 2026, the picture is a market where deal count has thinned and cheque size has concentrated. Investors are still writing, and they are writing fewer, larger cheques into AI-powered tooling.

Regional Distribution

Where the creator economy sits on the map

North America holds the largest share of the global creator economy at 33.2% by Grand View Research's measure, with other 2026 reads placing it at 33–37%. The US market alone was worth roughly $50.9 billion in 2024. Europe accounts for around 22%, near $41 billion in 2026. Asia-Pacific is the fastest-growing region in essentially every 2026 forecast, carried by mobile-first adoption and large young populations across India, Indonesia, and South Korea.

By creator population, the US and India lead by a wide margin, followed by Brazil and Indonesia.

Region determines rate as much as niche does. North America and Europe carry the highest CPMs. Asia-Pacific runs on volume. A brand running a global program is paying materially different prices into materially different tax systems on the same campaign, which is where the second half of this report starts.

The Human Layer

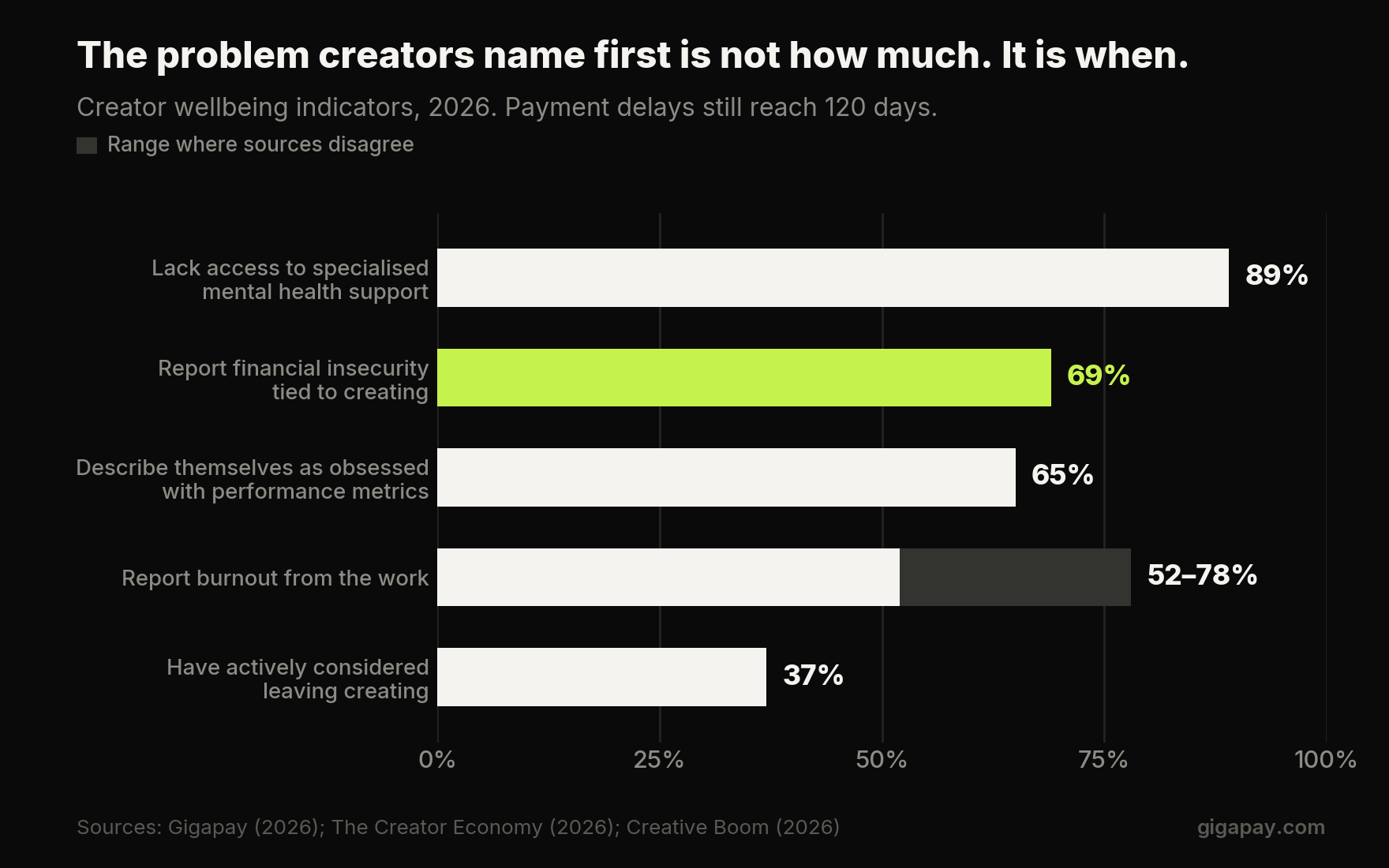

Why creators report burnout

The growth charts leave out the workforce, and the 2026 data on that workforce is difficult reading.

Gigapay's 2026 data puts creator burnout at 52–62%. The Creator Economy's reporting puts it at 78%. A broader creative-industry survey found 69% experienced burnout in the past 12 months, rising to 77% among mid-career creators. The range is wide because the definitions differ, and every source in it points the same way.

The rest of the picture:

- 69% report financial insecurity tied directly to creating.

- 65% describe themselves as obsessed with performance metrics.

- 37% have actively considered leaving.

- 89% lack access to specialised mental health support.

- Nearly half feel less financially secure than they did a year ago.

Financial insecurity outranks algorithm pressure at the top of most creator pain-point surveys, which is the finding worth sitting with. The problem creators name first is not how much they earn. It is not knowing when it arrives.

There are counterweights. The shift toward owned audiences, memberships, and direct monetisation is reducing platform dependency for the creators who can build it, and a support infrastructure of coaches, tools, and mental health resources is forming around the profession. Both trends are early.

The Payment and Compliance Layer

Getting paid still breaks

Payment delays of up to 120 days are routinely reported across the industry. A creator earning a healthy annual income can still be functionally insolvent in month three, and a brand with a four-month payment cycle is not a partner of choice regardless of what the brief says. The financial insecurity numbers above are, in significant part, a timing problem wearing a compensation problem's clothes.

What the rules require in 2026

Around 78% of US sponsored posts carry adequate disclosures, leaving roughly one in five exposed. UK non-compliance estimates run higher, between 34% and 43%.

On the creator side, self-employment tax of 15.3% sits on top of income tax, and 71% of creators do not realise that free products and brand trips count as taxable income.

Why this lands on finance, not marketing

None of the above appears in a campaign budget. All of it determines whether the campaign closes.

A brand running a global creator program pays across 65 or more countries at once. Each payee is a vendor record, a KYC check, a bank detail to verify, an invoice to process, and a tax obligation in a jurisdiction the finance team may never have filed in. At 50 creators a year, a person absorbs that. At 500, the process becomes the constraint on growth. At 5,000, it stops being a process at all.

Gigapay's own analysis of a brand running 600 creator collaborations a year puts the manual cost at roughly €139,590 and 840 admin hours, against ~€46,350 and 60 hours when the payment layer is handled as infrastructure. The ERP goes from 300+ individual vendor entries to one.

This is where the concentration data closes the loop. Micro and nano creators take 45.5% of spend and deliver 8–12% engagement against mega's sub-2%. The top 10% still capture 62% of brand payments. The gap between where the performance is and where the money goes is held open by administrative friction, and administrative friction is a solvable engineering problem rather than a law of the market.

What Comes Next

1. The middle class survives or the market stalls

45.6% of creators now earn $10,000–$100,000. That cohort exists because brand budgets moved down-market and social commerce created a genuine mid-tier income. It persists only if paying that cohort stays cheap. If administrative cost per payee climbs, budgets retreat to the top 10% and the middle disappears.

2. Owned revenue keeps compounding

Subscriptions are the fastest-growing channel by Grand View's segment data. Communities deliver 40% more recurring revenue and 3x retention. Creators prioritising savings jumped from 32% to 76% in a year. The professionalising creator is building something that does not depend on a campaign, and platforms will keep responding to that.

3. AI stops being a differentiator and becomes a floor

At 75% integration and 86% usage, AI is table stakes. The 40–60% price discount on pure AI content and the 15–30% discount on hybrid work suggest the market is already pricing human judgment as the scarce input rather than production capacity.

4. Consolidation continues

70 deals in six months, a $250 million dedicated holding company, and consultancies buying agencies. The independent middle of the creator services market is being bought.

What This Means By Role

If you run finance

Creator spend has crossed 2–3% of revenue for active DTC programs and now carries tax exposure across 43+ disclosure regimes, a 4.9% German levy that triggers on a single hire, and DAC7 reporting. The question is no longer whether to control it. It is whether the control mechanism blocks growth or enables it.

If you run marketing

The performance data says the money should be with nano and micro creators, and 45.5% of spend has already moved there. The constraint on going further is not creative and it is not budget. It is how many payees your finance process can absorb before it stops saying yes.

If you run operations

Vendor sprawl is the measurable version of this problem. 300+ ERP entries against one. 840 admin hours against 60. The delta is the scalability of the whole program.

Conclusion

Read the 2026 data together and one conclusion assembles itself.

The creator economy is large, growing between 10% and 23% a year depending on how you count it, and tilting steadily toward smaller creators who deliver better engagement at lower cost. The reward keeps concentrating at the top anyway, and it does so partly because paying a lot of small creators across a lot of countries is operationally painful in ways that no growth chart records.

The brands that win the next phase are the ones that remove that pain. When a company can pay a thousand creators across 65 countries instantly, through one vendor and one invoice, with DAC7, KSK, and KU14 reporting handled automatically, the arithmetic on micro and nano creators changes completely. The friction that pushes budgets toward a handful of large names stops existing, and the budget gets to go where the attention actually is.

The growth in this report is real. So is the friction underneath it. The gap between the two is where the next decade of the creator economy market share gets decided, and closing it is available now rather than on a roadmap.

Send your first batch payout the same day you sign.

FAQs:

1. How big is the creator economy in 2026?

Between $235 billion and $600 billion, depending on definition. Narrow measures counting direct creator revenue cluster at $250–325 billion, with Grand View Research projecting $310.37 billion. Broad measures including creator-driven ad spend, commerce, and tooling reach $400–600 billion. Grand View models growth to $1.35 trillion by 2033 at a 23.3% CAGR.

2. How many creators are there worldwide?

More than 200 million people create content in some economic sense, with SociaVault putting the 2026 figure near 250 million. Roughly 50 million work at it professionally or semi-professionally, and about 2 million earn six figures. Only 4–5% earn primary income from it.

3. How much does the average creator earn in 2026?

CreatorIQ puts the average at $44,293, but the average describes almost nobody. The median creator earns about $3,000 a year and 48.7% earn under $10,000. The fourteen-times gap between mean and median is the defining feature of creator pay.

4. Which platform pays creators the most?

YouTube long-form pays the most per view at $2–$12+ per 1,000 views, reaching $20+ in finance and tech niches. YouTube Shorts pays $0.01–$0.13 and TikTok Creator Rewards pays $0.40–$1.00, so creators on those platforms rely on brand deals and commerce instead. YouTube's total 2026 payouts are estimated around $25 billion.

5. Which niche pays the highest CPM?

Finance and FinTech, at roughly $40–$80 CPM, because those audiences convert into high-value customers. Health and medical follows at $30–$60, beauty and fashion has dropped to $20–$40 on saturation, and gaming sits lowest at $8–$18.

.jpg)